Municipal museums and related cultural institutions often have greater capacity than non-municipal museums because of the non financial supports municipal structures provide. Examples might include IT services, human resources, and lawn maintenance. Most importantly, municipal institutions are often housed in municipal buildings. As a result, they do not have to pay for utilities, maintenance and property tax.

Property tax can be a huge expense for museums and other cultural organizations (particularly non profit ones). For example, an article in the Canadian Museums Association’s Museogramme June/July 1991 issue discusses cut backs on staff, programs and hours at the Art Gallery of Hamilton. At the time, they were paying $300,000 in property taxes, leaving little for maintenance or preservation.

Within this case study post, I examine the MacBride Museum’s relationship with the City of Whitehorse to argue property tax abatement is a form of cultural policy, which has a major influence on the community museum sector. Petitioning municipalities for property tax exemptions is a significant form of cultural policy advocacy.

Whitehorse and the MacBride Museum

As part of the Dawson City Museum Project, I have been reading through the Yukon Historical and Museums Association’s (YHMA) newsletters. I talk about how useful museum association newsletters are to cultural policy research in another post (here).

As the YHMA’s Fall 2013 Newsletter, a few CBC articles (here, here, and here), and the MacBride Museum’s website describe:

1950s: The MacBride Museum opens. It did not (and has never) paid property taxes.

Mid 1990s: The City of Whitehorse provides non profits (including museums) with tax exemptions (100%).

2013: The City proposes a modification to the exemptions, planning to cover only 88% of the property tax payment.

The YHMA began sharing concerns, opposing the proposal through the radio, television, and papers.

The City’s proposal was voted down.

2014: The City reintroduces the proposal and it passes.

2015: The City passes an amendment that if the museum holds the title for their land, it would not be taxed. This exemption only applies to the MacBride Museum (and not the Transportation or Old Log Church museums).

2016: The MacBride Museum begins a planned expansion and confirms the exemption would continue to apply to their larger space.

2018: The City sends the MacBride Museum a bill for property tax after the assessed value of the museum’s property increased. The Museum’s annual property taxes had increased from about 30,000 to 71,000.

The City of Whitehorse argues the MacBride Museum is now ineligible for tax abatement because it has a cap of $50,000 on annual grants to a single organization. The MacBride Museum argues the 2015 amendment is not contingent on the size of the tax.

As of July 2021, property taxes and whether the MacBride is exempt seems to still be a point of contention. The MacBribe and YHMA have posted related content, showing advocacy in action.

- The YHMA has:

- The MacBride Museum has (most of these points are visible on their website – here):

- Asked for signatures on a petition and letters of support from other organizations

- Made a submission to City Council

- Correspondeded with the City

- Articulated an argument as to why they should not pay taxes

- Answered questions people may have about the issue simply and clearly. There are a number of questions and answers, but here is the first page:

Other Examples

As seen in the Yukon example, provincial governments often say non profits museums and other cultural organizations (or those registered as charities) can be exempt from property taxes. They allow municipalities to impose additional requirements, indicating the exemption is simply a possibility. Here are a couple of examples:

Alberta

A guide on property tax explains the exemption for museums and other cultural organizations. Notably, municipalities may impose additional requirements:

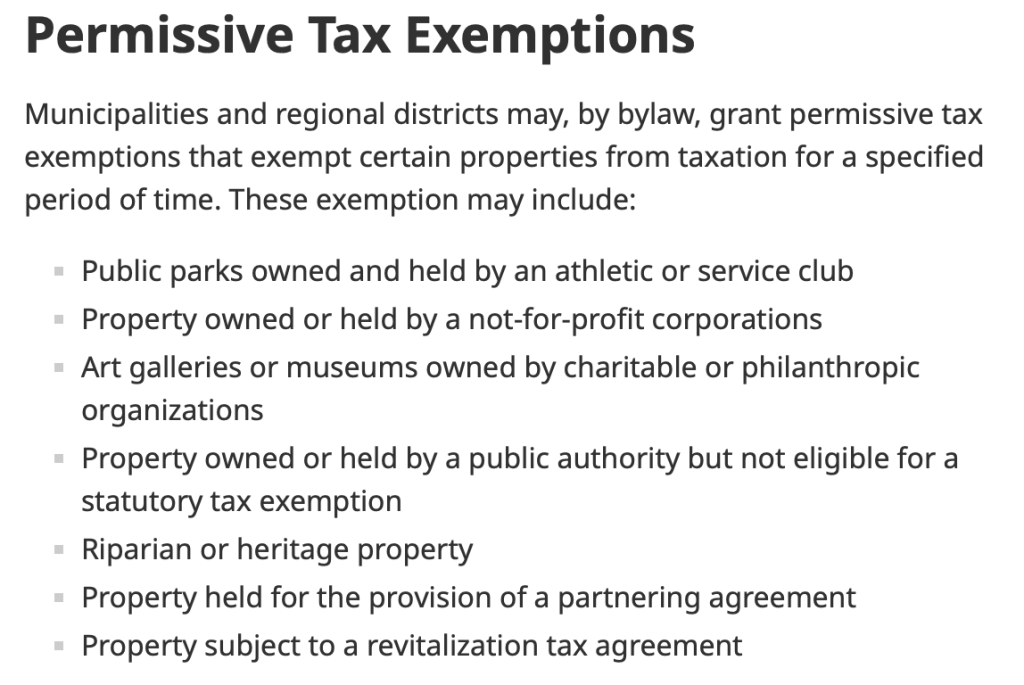

British Columbia

Provincial guidelines note museums owned by a charitable organization may be eligible for property tax exemption:

Saskatchewan

Under The Cities Act museums are not exempt from property taxes. However, they can be. In Saskatoon, for example, museums can apply for relief through the Culture Grant Program. They are not always successful! Click here for an example where the museum was not immediately successful but the City staff were committed to helping the organization meet requirements in the future.

Municipalities

As you can see, municipalities generally decide whether museums are exempt from property taxes in what is now known as Canada. As such, there is a lot of variance across the country. Part of the YHMA’s argument for the MacBride Museum is that most municipalities exempt museums. Here is a screenshot of their position with information on two municipalities:

Questions

To summarize, municipal tax exemptions are a significant form of cultural policy, requiring advocacy and attention, within what is now known as Canada. They demonstrate the important of advocacy at the municipal level (in addition to provincial / territorial, federal, and possibly First Nation).

Do you agree? Can you think of other significant examples?